Why Expanding Your Roofing Business to Hail-Prone Areas is a Smart Move

If you’re in the roofing business and thinking about growing your company or expanding to a new market, let’s have a little chat about why targeting areas with frequent hail storms might just be the golden ticket you’ve been looking for. Trust me, there’s a lot more to this than just bad weather—it’s about opportunity, profitability, and making your life a whole lot easier… well… kinda.

Why Hail-Prone Areas Are a Goldmine for Roofers

Let’s start with the obvious: hail storms wreak havoc on roofs. And when Mother Nature throws her icy fastballs, homeowners are left scrambling to repair the damage. And as you know… This is where you, the roofing expert, come in. But here’s the kicker—most of these repairs are covered by insurance. So knowledge isn’t just power… it’s profit in this instance. That means you’re not chasing down homeowners to pay out of pocket; instead, you’re working with insurance companies to get the job done.

Insurance Restoration vs. Retail Roofing

Here’s the deal: retail roofing (where homeowners pay directly) can be a tough sell. You’re often competing on price, and let’s face it, not everyone has the budget for a new roof and customers end up getting multiple quotes (one of which is usually WAY low). But with insurance restoration, the game changes. Homeowners are more likely to move forward with repairs because their insurance is footing the bill. This makes the sales process smoother and faster, but only if you can handle the entire claim from start to finish.

In reality, shingles over 10 years old are usually discontinued, and “most” states require a shingle to “match” for a small repair… That means in some states, 1 storm damaged shingle could require a full roof replacement by state law.

“In hail-prone areas, insurance restoration work can be up to 50% more profitable” than retail roofing with gross profits ranging from 45 – 60% based on the policy.

Real-World Example

Take a state like Texas, for instance. It’s no stranger to hail storms, and insurance companies there are well-versed in handling claims. A roofing company that expanded into Dallas after a major hailstorm reported a 40% increase in revenue within six months. Why? Because they tapped into the insurance restoration market, understood the supplementation process, and ensured jobs were plentiful and payments were reliable.

Key Considerations When Expanding

Before you pack up your tools and head to the nearest hail-prone state, there are a few things to keep in mind:

1. Research State Insurance Policies

Not all states are created equal when it comes to insurance. Look for states with homeowner-friendly policies that make it easier to file and process claims. States like Colorado and Oklahoma, for example, have a high volume of hail storms and insurance systems that are relatively straightforward to navigate. If you’re thinking of moving to Florida and live on the beach while your team sells roofs… think again.. even though it’s a good state for storms, the policies aren’t as profitable as states in the mid-west or southern states (AK, TX, TN, MS, AL, GA).

2. Build Relationships with Insurance Adjusters

Insurance adjusters are your new best friends, not your enemies like many roofers claim. Establishing good relationships with them can make the claims process smoother and faster, I’ve had adjusters just walk up to one of our (my old company’s) jobs and buy the roof without even climbing it because they trusted our process. Attend local networking events or join industry associations to connect with adjusters in your target area.

3. Invest in Training

Insurance restoration work requires a different skill set than retail roofing. Make sure your team is trained in handling claims, understanding policy language, and documenting damage effectively. This will save you headaches down the road. See some of the details at HAAG – one of the leading engineering experts in storm damage assessment.

4. Be Ready for Cash-Flow Requirements

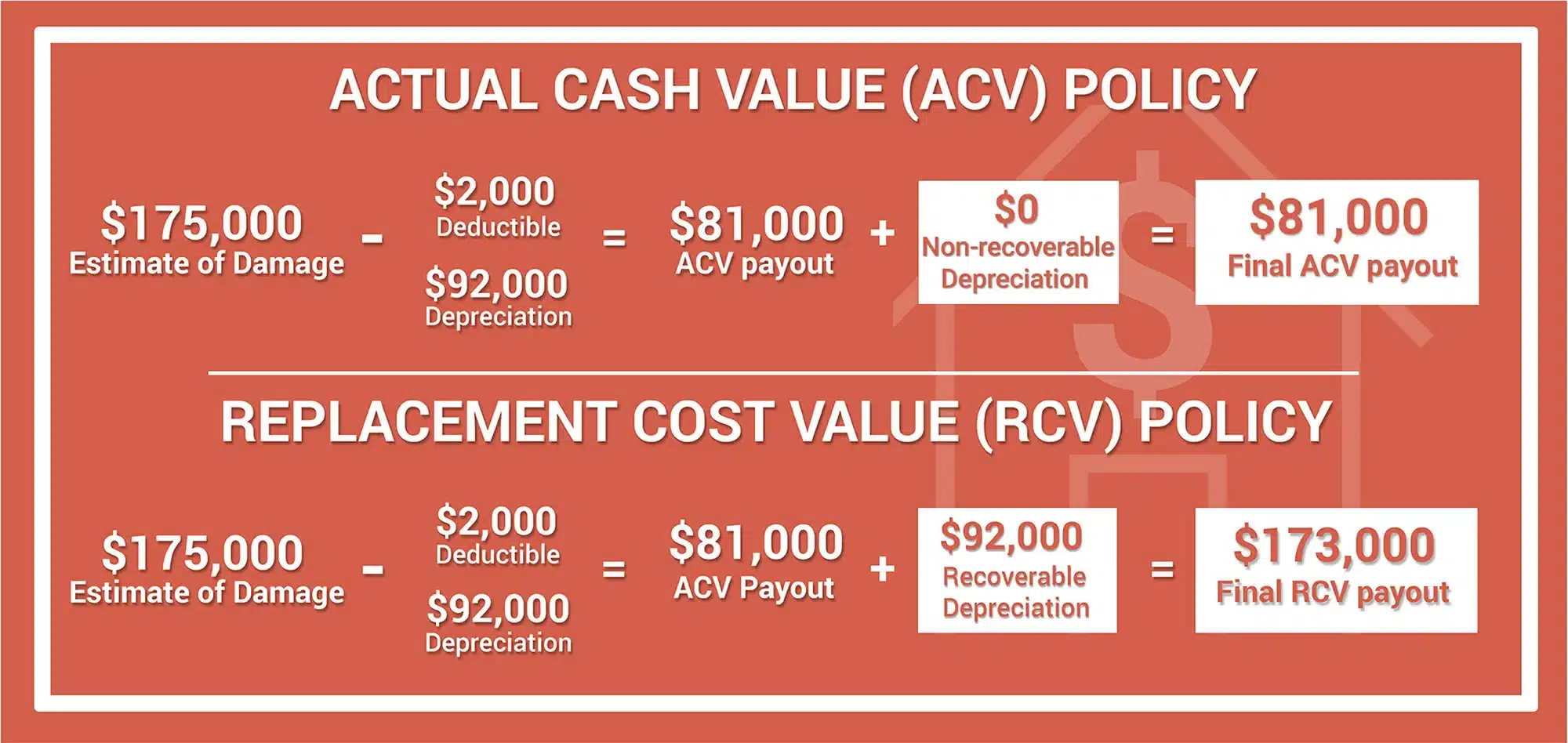

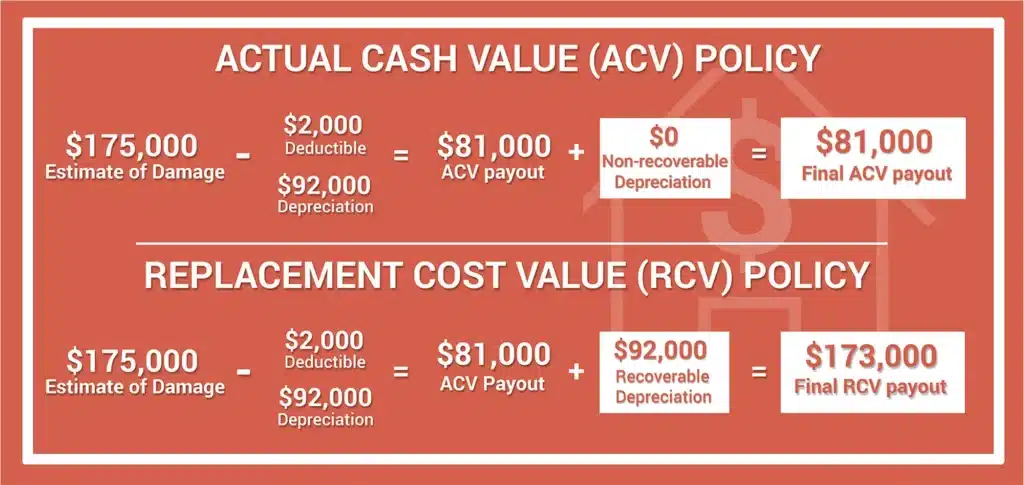

You can’t just collect a check in-full with insurance jobs. Typically, you’ll collect the ACV – which is usually 60% of the estimated cost to replace the roof, up-front. However. The remaining 40% usually needs to go through a supplementing process. So that usually means delays up to 60 days after the job is complete to collect in full. (If you’re good at it, you can get payment in 14 days).

Cost Considerations and Profit Potential

Let’s talk numbers. Expanding to a new area isn’t cheap, but the potential returns can make it well worth the investment.

Startup Costs

- Marketing and advertising: 4-8% of Expected Revenue

- Licensing and permits: $1,000–$3,000

- Training and certifications: $2,000–$5,000

- Recruiting: $3,000-$5,000 or existing employee move.

Profit Margins

In hail-prone areas, insurance restoration jobs often have much higher profit margins than retail roofing. On average, you can expect a 45-65% profit margin per job, compared to 20–30% for retail work. Plus, the volume of work in these areas when a storm does happen, can significantly boost your bottom line.

Ready to Expand? Here’s Your Next Step

So, are you ready to take your roofing business to the next level? Expanding into hail-prone areas can be a game-changer, but it’s important to do your homework first. Research your target market, build relationships, and invest in the right training. With a little planning, you’ll be well on your way to growing a thriving, profitable business.

Have questions or need advice? Drop a comment below or reach out—I’d love to hear from you and help you on your journey!